ChatGPT Market Share 2026: Free Look at the AI Landscape

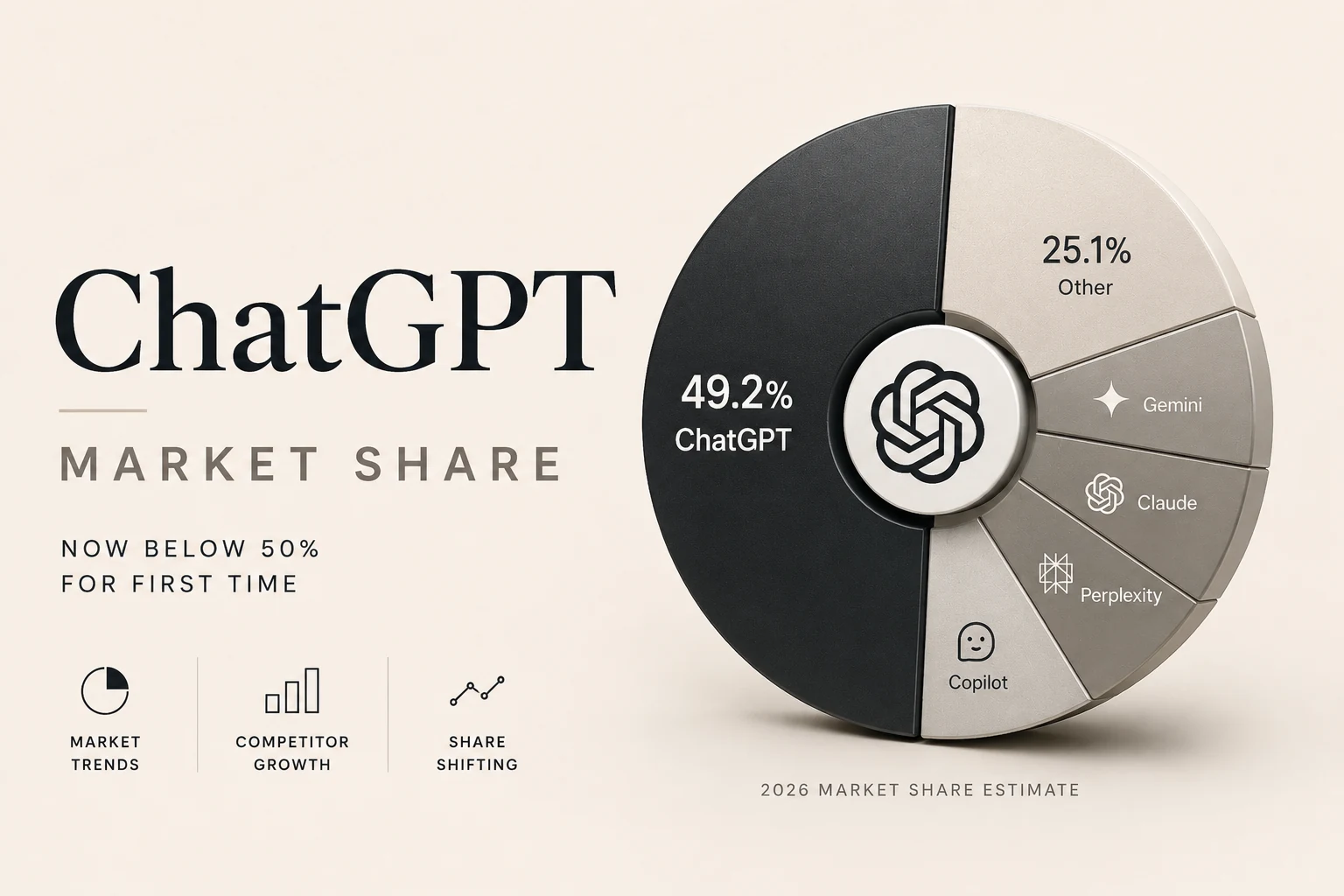

The chatgpt market share 2026 is 46.4%, slipping below the 50% threshold for the first time. Sensor Tower’s May 2026 report shows Gemini at 27.7% and Claude at 10.3%, reshaping the AI assistant landscape.

chatgpt market share 2026: key takeaways

- Overall position: ChatGPT remains the largest AI assistant with roughly 1.1 billion monthly active users, but its share has fallen from 65.3% in Dec 2024 to 46.4% in May 2026.

- Growth of rivals: Gemini’s user base grew from 533 million to 662 million in five months, while Claude jumped from about 3% to 10.3% of the market – a 452 % YoY increase.

- Market dynamics: The top three assistants (ChatGPT, Gemini, Claude) now control about 84 % of the global AI‑assistant market, leaving the rest split among single‑digit players.

These points illustrate why the chatgpt market share 2026 figure matters: it signals a shift from a near‑monopoly to a three‑way race, with direct implications for pricing, feature rollout, and user choice.

How is chatgpt market share 2026 evolving compared to competitors?

Understanding the trend requires looking at both metrics and distribution channels.

- Metric clarity – Sensor Tower’s “True Audience” metric counts unique users across mobile apps, mobile web, and desktop web for AI‑assistant applications only. It differs from web‑traffic or revenue‑based measures that often show higher ChatGPT percentages.

- Distribution advantage – Gemini’s integration into Android, Google Search, Gmail, and Docs gives it default exposure to billions of users. Claude’s focus on enterprise APIs drives higher paid conversion rates (≈13 % vs. the 2‑5 % typical for consumer software).

- User growth vs. share loss – Although the chatgpt market share 2026 dropped, absolute user numbers kept climbing, reaching the 1.1 billion milestone faster than TikTok or Instagram. The pie is simply growing faster than ChatGPT can capture.

According to Statista, global AI software market revenue reached $120 billion in 2025, a figure that underlines the expanding “pie” that all assistants are trying to slice Statista AI Market. The National Institute of Standards and Technology (NIST) also reports a 42 % YoY increase in enterprise AI adoption during 2025 NIST AI Adoption, reinforcing why new entrants can grow quickly.

Why Gemini is gaining on ChatGPT

Gemini’s surge is less about model superiority and more about where the model lives. The following bullet list captures the three core levers:

- Android OS integration – Gemini replaces Google Assistant as the default voice assistant on the world’s most‑used mobile platform, giving it instant reach on billions of devices.

- Google ecosystem wiring – Tight coupling with Search, Gmail, Docs, and Workspace means users can invoke Gemini with a single tap, without installing a separate app.

- Free‑tier accessibility – A generous free tier tied to a Google account lowers barriers in markets where Android dominates, especially in Europe and Asia.

These distribution advantages translate into raw numbers: Gemini added 129 million users between Dec 2025 and May 2026, while ChatGPT added roughly 80 million in the same period.

Claude’s niche power and its impact on market share

Claude’s chatgpt market share 2026 footprint may look modest at 10.3%, but its influence is amplified by higher monetization and a developer‑centric user base.

- Enterprise focus – Claude is heavily used through APIs on platforms like Amazon Bedrock and Google Cloud Vertex AI, where paid conversion rates hover around 13 %, far above the consumer average.

- Revenue per user – In the U.S., Claude’s average revenue per user (ARPU) rose from $0.50 in Sep 2025 to $2.76 by May 2026, roughly 1.5× ChatGPT’s ARPU in the same market.

- Developer adoption – Surveys show that 42 % of professional developers preferred Claude for code‑generation tasks in 2026, compared with 28 % for ChatGPT.

These factors mean that while Claude’s raw user share is smaller, its share of value within the AI‑assistant ecosystem is disproportionately large.

The smaller players: context and realistic expectations

Below the top three, the market fragments into single‑digit slices. Understanding each helps set realistic expectations for users and investors.

| Assistant | Approx. Share (May 2026) | Notable Strength |

|---|---|---|

| Grok (xAI) | 3.3 % | Conversational style, tied to X platform |

| DeepSeek | 3.2 % | Strong time‑spent metrics in China |

| Perplexity | 2.8 % | Real‑time web citations, answer‑engine focus |

| Meta AI | 2.5 % | Embedded in WhatsApp/Instagram, incidental use |

| Microsoft Copilot | 1.6 % | Enterprise productivity suite integration |

Even with massive distribution (e.g., Meta AI’s presence in billions of social‑media sessions), these assistants hold modest chatgpt market share 2026‑style percentages because users rarely open a dedicated assistant app when the functionality is baked into another service.

Practical implications for everyday users

The shifting chatgpt market share 2026 landscape creates tangible benefits:

- Better free tiers – Competition forces each provider to improve free‑level features, storage limits, and response speed.

- Task‑specific selection – Gemini excels for Android‑centric workflows, Claude shines for coding and long‑form analysis, while ChatGPT remains the most versatile with the largest plugin ecosystem.

- Cross‑tool workflows – RunFreeTools lets you experiment without juggling logins. Use our free AI Blog Writer to draft content, then run the result through the AI Content Detector to ensure originality.

By treating AI assistants as interchangeable tools rather than a single default, you can optimize cost, speed, and output quality.

What to watch in the rest of 2026

The AI‑assistant market remains fluid. Key signals to monitor include:

- Gemini’s distribution depth – Will Google push Gemini deeper into Chrome and Wear OS?

- Claude’s enterprise traction – Can Anthropic sustain its high ARPU as larger firms adopt competing APIs?

- Emergence of new entrants – Watch for any breakthrough from Grok or DeepSeek that could disrupt the top‑three balance.

- Regulatory developments – Potential EU AI Act rulings could affect how data is collected for “True Audience” metrics, altering reported shares.

Sensor Tower updates its State of AI report quarterly, so treat the May 2026 snapshot as a frame in an ongoing story rather than a final verdict.

Frequently asked questions

The decline reflects faster user growth for Gemini and Claude, not a loss of absolute users for ChatGPT. Sensor Tower’s True Audience metric shows ChatGPT at 46.4% in May 2026, while Gemini rose to 27.7% and Claude to 10.3%.

No. As of May 2026, ChatGPT still leads with 46.4% market share and over 1.1 billion monthly active users. Gemini holds 27.7% with 662 million users, making it the second‑largest assistant.

Claude’s focus on enterprise APIs, higher paid conversion (≈13 %), and strong developer adoption drove its share from ~3 % in 2025 to 10.3% in 2026—a 452 % year‑over‑year increase.

Not necessarily. Choose the assistant that fits your workflow: Gemini for Android‑centric tasks, Claude for coding or long documents, and ChatGPT for general‑purpose use. The competition simply gives you more free options and better features.

RunFreeTools offers a suite of free AI utilities that work directly in your browser. Try the **[AI Blog Writer](/ai-blog-writer)** for drafting, then verify output with the **[AI Content Detector](/ai-content-detector)**—no separate logins required.

Sources

Share this article

Send it to a teammate or save the link for later.

Related tools

Related articles

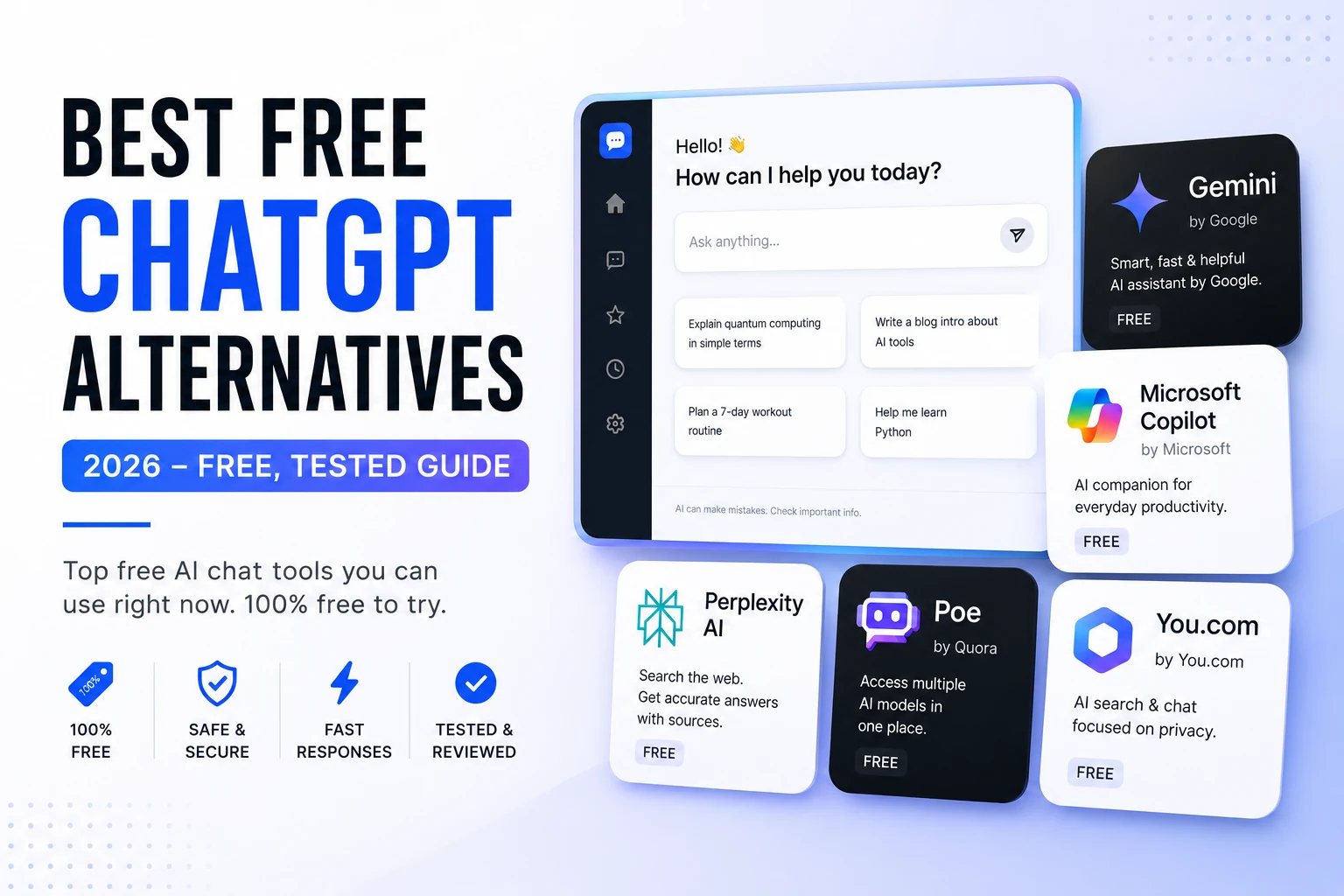

Best Free ChatGPT Alternatives 2026 – Free, Tested Guide

Discover the best ChatGPT alternatives in 2024. Compare Claude, Gemini, Perplexity, Copilot, Mistral, DeepSeek and more—free options, coding power, research

Read article

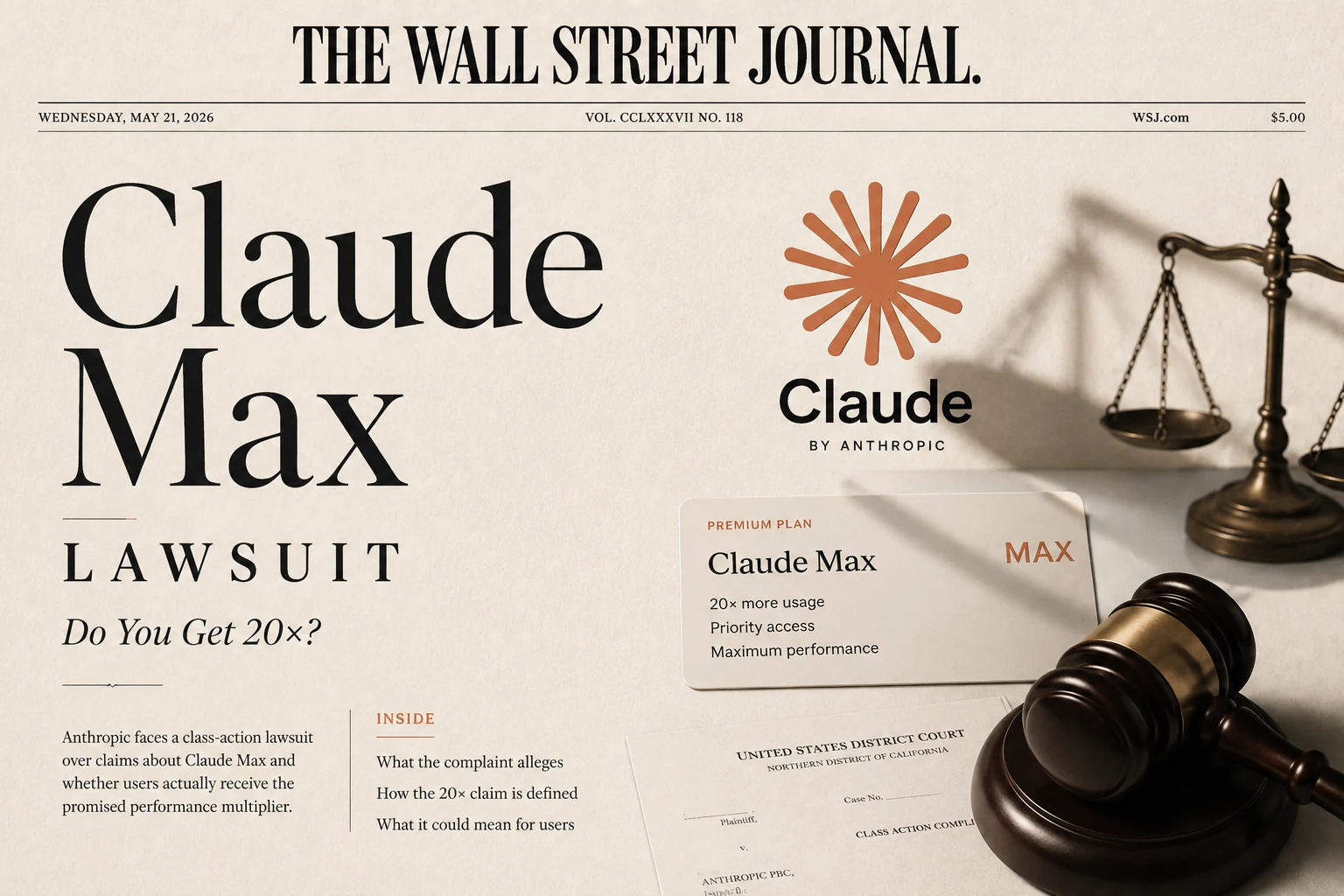

Anthropic Claude Max Lawsuit: Proven 20x Claims Explained

Anthropic Claude Max lawsuit says the 5x and 20x plans give far fewer tokens than advertised. See the claims, token limits, and if upgrading is worth it.

Read article

Free gpt-5.6 release date: Leaks, Predictions & Prep

Track the gpt-5.6 release date with leaked signals, prediction‑market odds, and official OpenAI updates. Learn rumored features and how to prepare today.

Read article